Beginning of the end or the end of the beginning? Fighting plastic pollution one bag at a time

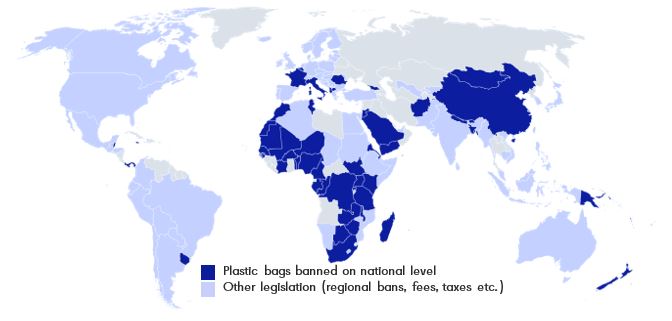

In the wave of the global trend of single-use plastic bag bans, China recently followed suit by banning the usage of all non-degradable bags gradually by 2025. The wealthiest cities, like Beijing and Shanghai, will face the ban already by the end of 2020. Low grammage plastic bags will be banned altogether, like many single-use plastic items.

Plastic bag bans usually target the bags’ (1) thickness threshold (2) plastics’ characteristics, such as biodegradability (3) entire plastic bag market, and are set on national regional or citywide level

THE GLOBAL SHOPPING BAG MARKET

The global shopping bag market size is estimated at more than 450 billion bags sold annually, with a solid annual growth of nearly 4% during this decade, or nearly 20 billion new bags annually. Plastic bags account for a lion’s share of this volume, around 80% of total shopping bag demand at current. Some 15% of the plastic bag volume consists of bioplastic bags, a segment with high growth potential, especially for biodegradable bioplastics, but still in a development stage facing challenges related to quality and competitiveness.

The major growth on the shopping bag market is expected in the multiuse bag segment, including nonwoven, jute and cotton bags. Paper bags are expected to grow inline with the market, retaining their share of close to 4% of all shopping bags.

GOOD, BAD AND UGLY PLASTIC

The downsides of plastic bags include their fossil raw-material content, long decomposition time and currently undeveloped recycling practices and facilities. These have led to severe ocean pollution in many areas where plastic collection and recycling is not properly managed, causing great visual harm and most notably being detrimental to marine life. The microplastics released to the environment in the breakdown process is also causing widespread public health concern.

The conventional plastic bag has, however, many benefits when compared to rivalling materials. These include competitive price, functionality, hygiene as well as low weight and space requirement. Taken that the end-of-life is adequately managed, the plastic bag performs well also in life-cycle assessments often standing out as the most sustainable alternative.

SUBSTITUTION TAKES MANY FORMS

Legislative initiatives by national governments to reduce or curb the use of single-use plastic bags have resulted in various forms of substitution: single-use to reusable; conventional plastics to other types of plastic material and; from plastics to other substituting materials. However, the first impact witnessed in the aftermath of a ban is, without exception, a radical drop in overall bag consumption when unnecessary and multi-layered packaging is avoided.

Efforts to reduce the use of plastic bags have seen mixed success. Previous trials in China have faltered when substituting materials have not been available in required volumes and consumers have not been willing to give up entrenched consumption habits overnight. Hence, in order to enable the substitution of conventional plastics or their more efficient recycling, the entire supply chain will need to act. The ability of different stakeholders to adjust to the new operating environment will determine whether plastic bags are slowly being wiped out or will, for example, be introduced to a patent-based return system ensuring no bags end up in landfills or nature but as recycled material for new bags.

Vision Hunters provides strategic advisory services for the forest industry and energy sectors. We assist leadership teams in making the smartest strategic choices to improve the outcome of their company in the future. We are highly experienced and result oriented and have advised many of the leading companies in our industry.